The

Caribbean Market Is Heating Up in More Ways Than

One

By

Parris Jordan

HVS International New York

Location

and History

The

Caribbean region consists of 32 countries comprising

hundreds of islands in the Caribbean Sea. Spanning

an area of almost one million square miles, these

islands are situated between Florida to the north

and Venezuela to the south.

The

Caribbean countries vary considerably in size with

the smallest country, Saba, measuring roughly five

square miles and the largest, Cuba, measuring approximately

42,800 square miles. The Caribbean was "discovered"

in 1492 during the first voyage of Christopher Columbus.

Throughout

the 16th century, the Caribbean islands grew in

importance to the Spanish empire, as Spain claimed

the entire Caribbean and created settlements on

the larger island colonies. As the Spanish empire

declined throughout the 17th and 18th centuries,

other European countries established colonies all

over the Caribbean region.

The

Caribbean colonies were very important to the European

nations because the plantations that were established

there generated great wealth for the "mother

country." Sugar was the main crop produced

throughout the Caribbean region and by the 1800s

plantations on the Caribbean islands produced 90%

of the sugar that was consumed in Europe.

To

satisfy the enormous manpower requirements of the

plantation system, a vast number of Africans slaves

were imported throughout the 18th century. Following

the abolition of slavery, the colonies turned to

imported indentured labor from India, China, and

the East Indies to meet the demands for labor.

For

the most part, the Caribbean islands tend to share

a similar geography, culture, and history despite

speaking the different languages of the European

nations that colonized the respective Caribbean

countries. Overall, the Caribbean nations were colonized

by either Spain, France, Holland, Britain, or Denmark

during their history.

Today,

most of the Caribbean nations have gained their

independence while some of the smaller nations are

still colonies of European powers (the U.S. Virgin

Islands were originally colonies of Denmark until

1916, prior to selling sovereignty to the U.S.,

which still governs them).

The

following table lists the Caribbean countries by

national language.

Table

1 - List of Caribbean Countries Categorized by Native

Language

English

Anguilla

Antigua and Barbuda

Bahamas

Barbados

Belize

Bermuda

British Virgin Islands

Cayman Islands

Dominica

Grenada

Guyana

Jamaica

Monsterrat

St. Kitts and Nevis

St. Lucia

St. Vincent and the Grenadines

Trinidad and Tobago

Turks and Caicos Islands

U.S. Virgin Islands

Dutch

Aruba

Bonaire

Curacao

St. Eustatius

St. Maarten

Suriname

Spanish

Cuba

Dominican Republic

Puerto Rico

French

Guadeloupe and St. Barts

Haiti

Martinique

St. Martin

Map

of the Caribbean

The Caribbean islands possess limited natural resources.

Only the islands of Jamaica (bauxite and gypsum)

and Trinidad (petroleum, pitch, and natural gas)

contain notable natural resources. However, the

Caribbean region benefits tremendously from the

natural beauty of the region's spectacular beaches,

exotic wildlife, cultural diversity, warm tropical

weather, and numerous festivals.

These

benefits, which appeal to tourists from all over

the world, as well as the history associated with

the European nations and proximity to the United

States, are the main reasons for the Caribbean's

transition from an economy that was historically

heavily dependent on agriculture throughout the

18th through 20th centuries, to a region that is

currently reliant on the travel and tourism industry.

Importance

of Tourism to the Caribbean Region

Tourism

in the Caribbean is not only important, it is also

critical for the economic survival of the region.

According to the World Travel and Tourism Council,

the Caribbean is clearly the most tourism intensive

region in the world.

Travel

and tourism currently account for 15.4% of the total

gross domestic product and generate 15.5% of total

employment in the Caribbean. The industry's vital

role as a generator of wealth and employment across

all parts of the region is indisputable as it acts

as a catalyst for growth in other areas such as

agriculture, construction, and manufacturing. Overall,

the tourism industry generates over $20 billion

a year for the region and provides more jobs than

any other industry.

Some

islands are more dependent on tourism than others.

For example, the British Virgin Islands, Antigua,

and Barbuda owe more than 75% of their economies

to travel and tourism, while four other Caribbean

nations owe between 50-75% of their economies to

travel and tourism.

Another

important indicator of the travel and tourism industry

to the region is employment. The World Travel and

Tourism Council estimates that of all the jobs generated

in the British Virgin Islands, Antigua, and Barbuda,

95% of employment is directly or indirectly produced

by the travel and tourism industry, while roughly

80% of jobs created in Anguilla are a direct result

of travel and tourism.

Overall,

in 2005, the Caribbean travel and tourism economy

employment is estimated at roundly 2.4 million jobs,

15.5% of employment, or one in every 6.6 jobs. These

statistics clearly indicate the islands' heavy dependency

on the tourism industry, a circumstance that is

considered to present both positive and negative

aspects to the region.

Impact

of 2001 Terrorist Attacks on Caribbean Tourism

On a positive note, the Caribbean region enhanced

its position as a preferred tourist destination

to the North American and European markets during

the 1990s. In fact, the Caribbean region enjoyed

a 5.1% growth rate in tourist arrivals during the

decade of the 1990s while the overall global growth

rate was 4.8%.

However, from July 1999 to July 2001, the Caribbean

region's growth rate declined to 4.3%, lower than

the overall global growth rate for tourist arrivals.

The most obvious and influential negative factor

of the Caribbean region's dependence on tourism

renders the islands' economy extremely susceptible

to fluctuations in the level of tourism.

As tourism is generally tied to the levels of discretionary

income of the population that constitutes the destination's

primary market area, the economy of the islands

is directly influenced by fluctuations in the U.S.

and European economies.

By September 2001, tourist arrivals to the Caribbean

region were already declining and the 2001 global

economic recession and terrorist attacks on the

U.S. only exacerbated the situation throughout the

Caribbean region.

The negative impact of the terrorist attacks led

to the loss of jobs, declines in discretionary income

levels, and consequent declines in the tourism industry

throughout the United States and popular U.S. and

European destination locations, including the Caribbean

islands.

The World Tourism Organization estimates the total

number of international arrivals to the Caribbean

declined to 16.1 million in 2002, down from its

historical peak of 17.2 million in 2000. The 2001

terrorist attacks severely impacted the Caribbean

region, as hotel occupancy levels declined, many

Caribbean airlines, hotels, and restaurants were

forced to reduce employee hours and, in many cases,

cut jobs.

Although the effects on the Caribbean market were

dramatic and immediate, the market recovered quickly

and by 2003, total visitor arrivals posted a record

high of 17.3 million.

Recovery of the

Caribbean Market

By 2003, the Caribbean recorded healthy gains in

tourist arrivals and tourism receipts. This trend

continued into 2004 as the Caribbean market rebounded

quickly following the two disappointing years of

2001 and 2002.

The market's recovery can be attributed to a combination

of factors. With the ongoing "War on Terrorism,"

U.S. travelers' perceived level of security is reportedly

higher in the Caribbean islands than in other offshore

destinations.

As many parts of the world appear to present real

or perceived terrorist threats to the U.S. market,

the Caribbean region continues to benefit through

its positioning as a region that is safe and secure

for vacationers and family. Moreover, according

to the World Travel and Tourism Council, some tourists

from the United States still appear reluctant to

travel further afield as they are nervous about

the hostile reception they feel they may receive

from European and Asian nations as result of the

U.S. government's stance on Iraq.

Another reason for the market's recovery is the

relative strength of the Euro versus the U.S. dollar.

The strength of the Euro presents opportunities

for European tourists to travel to the Caribbean

as prices may appear more attractive, thus creating

greater value for the European tourists.

Additionally, the islands' history that is forever

linked to various European nations through colonialization

continues to be a main driver for visitation to

the respective former island colonies by residents

from the European "mother country."

To further illustrate the recovery of the Caribbean

market, the following table presents hotel performance

in the region as complied by Smith Travel Research

(STR), an independent research firm that compiles

data on the lodging industry; its published data

is routinely used by typical hotel buyers.

STR has compiled historical supply and demand data

for selected hotels within the Caribbean market.

This information is presented in different formats

in the following tables, along with the marketwide

occupancy, average rate, and rooms revenue per available

room (RevPAR) for fifty-six branded luxury, upper

upscale, and upscale hotels with a room count of

650 units or less. RevPAR is calculated by multiplying

occupancy by average rate, and provides an indication

of how well rooms revenue is being maximized.

Table

2 - Historical Supply and Demand Trends (STR)

Table

3 - Historical Supply and Demand Trends (STR) -

Average Rate and Occupancy, Monthly Data 1999-2005

Table

4 - Historical Supply and Demand Trends (STR) -

Average Rate, Occupancy, and RevPAR, Monthly Data

2000 - Year-to-Date February 2006

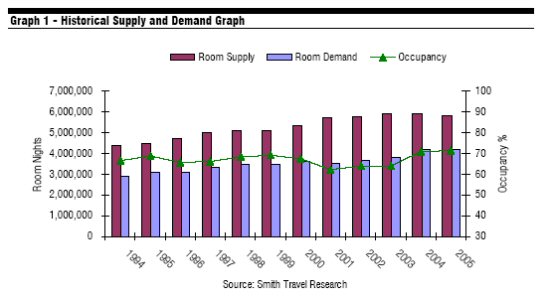

Graph

1 - Historical Supply and Demand Graph

As illustrated by the preceding table, the average

room count of the aggregate Caribbean hotels increased

notably between 1994 and 2005. In 2001, the market

exhibited a substantial increase of 6.5%.

During the period 2002 to 2003, the market's overall

room count registered marginal increases, while

the total room count was reduced slightly in 2004

and 2005, due to the reduction in room supply of

a few hotels following the damages caused by the

impact of the 2004 and 2005 hurricane season. Overall,

occupied room nights increased from 2,932,760 in

1994 to 4,175,685 in 2005.

Lodging demand in the subject market increased at

an average annual compounded rate of 3.3% between

1994 and 2005. During the period 1997 through 2000,

the market exhibited strong growth in terms of occupied

room nights. In 2001, occupied room nights decreased

by 1.7%.

The decline in occupied room nights was a direct

result of the negative impacts of the September

11 terrorist attacks on the travel industry, and

was further compounded by the global economic recession.

In particular, the Caribbean's tourism industry,

which relies heavily on leisure demand, was hampered

by the reduction in air travel following these attacks.

In subsequent years, the market gradually showed

signs of recovery, as marketwide occupied room nights

posted increases of 3.3% and 3.7%, in 2002 and 2003,

respectively.

In 2004, the market continued to improve, however,

at a much faster pace as exhibited by a significant

increase of 10.5% in accommodated room nights, which

is indicative of the gradually improving economic

climate and the underlying strength of the Caribbean

lodging market and is primarily due to the increase

in leisure travel. Occupied room nights remained

fairly stable in 2005 and year-to-date figures through

February 2006, compared to the same period last

year, indicate a further increase in marketwide

occupied room nights, by 2.0%.

Changes in occupancy levels were reflective of the

market's historical supply and demand dynamics.

Prior to 2001, occupancy levels were typically in

the middle to high 60% range, peaking at 68.9% in

1999.

Based on our analysis of monthly market data and

discussions with Caribbean hotel operators, occupancy

levels in the Caribbean lodging market actually

began to decline in September 1999. This downward

trend continued into 2001 and was further exacerbated

by the global economic recession and the 2001 terrorist

attacks, as marketwide occupancy posted a historical

low of 62.1%.

In subsequent years, the market exhibited successive

increases in occupancy levels with moderate increases

in 2002 and 2003. With no increases in supply in

2004, marketwide occupancy rebounded, posting a

significant increase of 10.8%. The 10.8% increase

in occupancy levels in 2004 is reflective of the

recovery of the Caribbean market.

These increases were due to the popularity of the

Caribbean market as leisure travelers visited the

region following the recovering economies and rebound

of the travel industry.

This trend continued into 2005, as marketwide occupancy

increased by 1.0%; at 71.5%, the resultant occupancy

was the highest during the period reviewed. Year-to-date

figures through February 2006, compared to the same

period last year, show a continuation of the increasing

trend, as marketwide occupancy increased 1.7%.

Marketwide average rate fluctuated between 1994

and 2005. In absolute terms, average rate increased

$45.73 from 1994 to 2005. Notably, marketwide average

rate declined in 2001 and 2002, as hotels in the

subject market began to use price as a marketing

tool, in an effort to limit occupancy losses incurred

by the decline in occupancy levels.

The economic downturn, the terrorist attacks of

September 11, 2001, and the additions to supply

intensified competition in the subject market, compelling

management teams to implement price discounts in

an attempt to sustain occupancy levels.

As a result, marketwide average rate decreased by

2.8% in 2001. This downward trend continued into

2002, albeit at an accelerated pace, decreasing

by 4.5%. An analysis of the monthly data reveals

that this trend began to reverse in late 2002 and

by 2003, the market showed signs of recovery, as

average rate increased by 1.8%.

The recovery continued at an accelerated pace into

2004, as marketwide average rate increased notably,

by 6.1%. In 2005, the market continued to exhibit

substantial marketwide average rate growth as average

rate increased by 8.2%.

Year-to-date figures through February 2006, compared

to the same period last year, indicate a continuation

of this trend, as marketwide average rate increased

by 6.3%. An analysis of marketwide monthly average

rate data shows that in absolute terms, marketwide

average rate increased by $9.38 in January 2006,

accelerating to a $22.40 increase in February 2006,

compared to the same period last year.

According to local hotel operators, these healthy

rate increases were driven substantially by strong

weekday and weekend demand from the leisure segment.

The significant marketwide average rate increases

bode well for the Caribbean lodging market.

RevPAR reflects the dynamics of occupancy and average

rate. The underlying strength of the local lodging

market is clearly indicated by the substantial increases

in RevPAR growth from 2003 to 2005. RevPAR increased

continuously throughout the three-year period, posting

significant increases of 17.6% in 2004 and 9.3%

in 2005.

Year-to-date figures through February 2006, compared

to the same period last year, show a continuation

of this trend as RevPAR increased substantially

by 8.1%. These increases are reflective of the strength

of the Caribbean lodging market and one of the main

reasons that is encouraging further hotel development,

as will be detailed later in this narrative.

Seasonality

Despite the fairly stable climate, the Caribbean

market shows a significant level of seasonality

throughout the year, generally tied to the climate

in the northern United States and Europe, the points

of origin for most tourists to the region.

Seasonality is represented by strong occupancies

and average rates throughout the winter season,

which are offset by lower occupancies and highly

discounted rates in the months of September and

October.

In addition to the increased risk of hurricanes

in September and October, the profound seasonality

pattern of the Caribbean islands comes as a result

of the region's dependence on leisure travel.

Compared to destinations such as Florida or Hawaii,

the Caribbean islands have been less successful

in attracting group demand, which typically helps

to smooth the seasonality of demand. The seasonality

patterns of the subject market are shown in the

following table.

Table

5 - Seasonality

The

subject market's high season incorporates a five-month

period extending from December through April, when

the tourist activity in the area peaks. As exhibited

in the preceding table, occupancy levels in the

high season increased from the mid-60% range from

2001 to 2003, to a high of 75% in 2005, significantly

higher than pre-2001 high of 70.1% in 1999.

Discussions with local hotel operators reveal that

sell-out nights are often recorded, and a certain

amount of patronage has to be turned away.

The substantial demand compression also enables

hoteliers to achieve high average rates; in 2003,

the average rate in the high season amounted to

$221.44. However, as the market continued to strengthen,

marketwide high season average rates increased substantially

in 2004 and 2005 reaching $248.74 in 2005.

As previously mentioned, year-to-date figures through

February 2006, which represent two of the high season

months, show a continuation of average rate growth.

The months of May through August, and November constitute

the market's shoulder seasons. During the period

2001 through 2003, the market recorded occupancy

levels in the middle to high 60% range. In 2004

and 2005, the market exhibited increases in occupancy

and average rate above the benchmark year, 1999.

During the shoulder months, some of the Caribbean

hotel operators pursue the tour group segment more

aggressively, which typically generates less lucrative

business, but provides a relatively solid base of

occupancy. In 2005, marketwide average rate in the

shoulder season was positioned at $184.86, roughly

$64.00 below that prevailing in the high season

with occupancy levels slightly lower than the high

season.

The low season in the Caribbean comprises the months

of September and October, when the risk of hurricanes

increases sharply. During 2005, the occupancy level

in the low season was 57.6%.

The 2005 low season occupancy level was slightly

lower than levels recorded in 1999 and 2000, due

to the impact of 2005 hurricane season which produced

a record number of hurricanes and caused damage

to many of the Caribbean islands.

The lack of demand compression during this period

is also reflected in the marketwide average rate,

which, at $162.30 in 2005, was roughly $86.00 less

than that prevailing in the high season. In 2005,

RevPAR in the low season was only ±50% of

that recorded in the high season.

The seasonal character of the market greatly impacts

the performance of lodging facilities as the healthy

annual occupancies of properties illustrate the

strength of the market. In strong lodging markets,

annual occupancies above 70% indicate that an area

is frequently selling out its rooms, and therefore,

a portion of demand is most likely turned away.

As a new hotel enters a competitive market, the

unaccommodated demand is absorbed by this addition

to supply. However, in a seasonal market, the unaccommodated

demand is turned away only during the peak season.

Therefore, the unaccommodated demand will help fill

the new property's rooms for only part of the year,

while the remainder of the year's low season demand

is aggressively pursued by the area's competitors

through the upgrading of facilities and aggressive

marketing techniques.

A common marketing technique employed in seasonal

lodging markets is the use of rate discounting during

the low season, thereby illustrating the impact

market seasonality has on the potential revenue-generating

capability of a lodging facility. In the Caribbean

market, occupancy levels during the shoulder season

are currently above 70% as well, which indicates

that demand is also being turned away during the

shoulder season.

Caribbean Lodging

Market - How Hot is it?

What does all this mean to potential developers?

A market that is highly seasonal, with annual marketwide

occupancies over 70%, shoulder season occupancies

over 70%, and marketwide average rate and RevPAR

continuing to post impressive gains. What it means

is the Caribbean market has become a "hot market."

Markets that demonstrate these characteristics are

very desirable to developers. As a result, a number

of new projects, primarily from the upscale, upper

upscale, and luxury U.S. brands have been approved

for development within the Caribbean market.

However, the new developments that are planned exhibit

a notable decline of stand-alone hotels, rather,

the trend seems to be geared toward developing new

hotels as part of an overall mixed-use project.

The new developments are scheduled to include some

or all of a variety of uses such as condominiums,

timeshare, fractionals, marinas, golf courses, and

spas.

Developers are reducing their investment risk through

the combination of these components, compared to

the development of each component separately. As

indicated by the table below, these mixed-use projects

that are scheduled for development are well-known

North American hotel brands.

These brands are a promise to customers that is

delivered through consistent actions and behavior

over time. The selection of these strong brands

is an attempt by developers to reduce the investment

risk because of the brands' proven track record

and name recognition. The table below shows a number

of mixed-use projects that have been approved for

development within the Caribbean region by some

of these major brands.

Table

6 - Proposed Hotel Projects

Why is the Caribbean Region Spurring this Development?

A combination of factors is responsible for the

current "boom" that is spurring further

investment and development in the Caribbean region.

As previously mentioned, the local lodging market

continues to exhibit substantial increases in RevPAR

with marketwide annual occupancies above 70%.

With the influx of foreign investment, particularly

from the United States seeking development opportunities

with higher yields, the Caribbean region, due to

its political stability and proximity to the United

States seems to be a logical choice for developers.

Moreover, many of the retiring baby boomer generation

are seeking vacation homes or a second residence

in a tropical destination other than a coastal U.S.

destination such as Florida or California. The Caribbean's

natural beauty, proximity to the U.S., and improved

airlift are seen by the baby boomers as attractive,

yet still less expensive than many other locations.

Conclusion

The Caribbean lodging market has rebounded from

the difficult years of 2001 and 2002 and continues

to post impressive gains that are attracting major

foreign investment into the region.

According to management representatives of Marriott

International, the Caribbean exceeded expectations,

as leisure travel continues to boom. Marriott International

anticipates significant additional expansion opportunities

in the region.

In the past, the local Caribbean countries' infrastructure

has improved tremendously, and as a result, has

facilitated the growth in tourism. Despite the profound

seasonality pattern of Caribbean visitation, the

market continues to attain overall annual occupancies

in excess of 70%.

The new mixed-use projects that are approved for

development include several components that will

help smooth out the impact of seasonality by increasing

occupancy during the low season. The introduction

of low cost carriers to the region will reduce the

cost of travel to the region, increase the awareness

of some of the lesser-known destinations, and continue

to improve airlift to the region.

As the Caribbean lodging market continues to expand,

the dynamics of hotel development in the region

are slowly changing as mixed-use projects that typically

include a residential component with a notable upscale

or luxury brand are becoming the norm.

Parris Jordan is a consultant with HVS International

New York. He can be reached at pjordan@hvsinternational.com,

516-248-8828, 372 Willis Ave., Mineola, NY 11501. For

the latest news in the hospitality industry, visit

his website at www.hvsinternational.com.